Open Banking API: Complete PSD2 Guide 2026

Understand Open Banking APIs, their advantages, integration strategies, and how they securely enable innovative financial services and collaboration

An open banking API is a secure, standardised interface that enables licensed third-party providers to access customer-authorised financial data and initiate payments directly from bank accounts. Governed by regulations like PSD2 and open banking standards worldwide, these APIs power innovations in payments, lending, personal finance, and fraud prevention.Govern and Monetize your Open Banking APIs with DigitalAPI, Book a demo!

What Exactly IS an Open Banking API?

An open banking API (Application Programming Interface) is a set of protocols and tools that allows banks to share customer financial data with authorised third-party providers (TPPs) securely and in real time. Think of it as a digital bridge: on one side sits the bank holding your financial data, and on the other side sits a fintech app that can use that data, with your explicit consent, to offer you better services.

But open banking APIs are not just about sharing data. They also enable third parties to initiate payments directly from customer bank accounts, bypassing traditional card networks entirely. This dual capability, data access, and payment initiation, is what makes open banking APIs transformative for the financial industry.

From Screen Scraping to Secure APIs

Before open banking APIs existed, fintechs relied on a practice called screen scraping. Users would hand over their bank login credentials to a third-party app, which would then log in to the bank on their behalf and extract (or "scrape") transaction data from the screen. This approach had serious problems:

- Security risk: Users shared their actual banking passwords with third parties.

- Fragility: If a bank changed its website layout, scrapers broke.

- No consent framework: Banks had no visibility into or control over who accessed customer data.

- No standardisation: Every bank had a different interface, making integration expensive.

Open banking APIs solved all of these problems by creating a standardised, secure, consent-driven mechanism for data sharing and payment initiation.

PSD2: The Regulatory Catalyst

The most significant driver of open banking was the European Union’s Revised Payment Services Directive (PSD2), which came into force in January 2018. PSD2 mandated that banks in the EU and EEA must provide licensed third parties with access to customer account data and payment initiation services through secure APIs.

PSD2 introduced two critical concepts:

- Account Information Services (AIS): Third parties can access account balances, transaction histories, and other financial data with customer consent.

- Payment Initiation Services (PIS): Third parties can initiate payments directly from a customer’s bank account, without needing a card.

PSD2 also mandated Strong Customer Authentication (SCA), requiring at least two of three authentication factors (something you know, have, or are) for online transactions, significantly boosting security.

Key Takeaway

Open banking APIs replaced insecure screen scraping with standardised, consent-based data sharing. PSD2 made this mandatory across Europe, and similar regulations are now spreading globally.

How Do Open Banking APIs Actually Work?

Open banking APIs follow a structured flow that ensures security and user consent at every step:

- Customer Consent: A user opts in to share their financial data or initiate a payment through a third-party application. Consent is granular: the user specifies what data to share and for how long.

- Authentication: The user authenticates with their bank using Strong Customer Authentication (SCA), typically through their banking app or a redirect to the bank’s secure portal.

- API Request: The third-party provider sends a standardised API request to the bank’s open banking endpoint, including the authorisation token.

- Data Retrieval / Payment Execution: The bank validates the request, checks authorisation, and returns the requested data (AIS) or executes the payment (PIS).

Ongoing Security: All communications are encrypted with TLS. Tokens expire and must be refreshed. Audit logs track every access event.

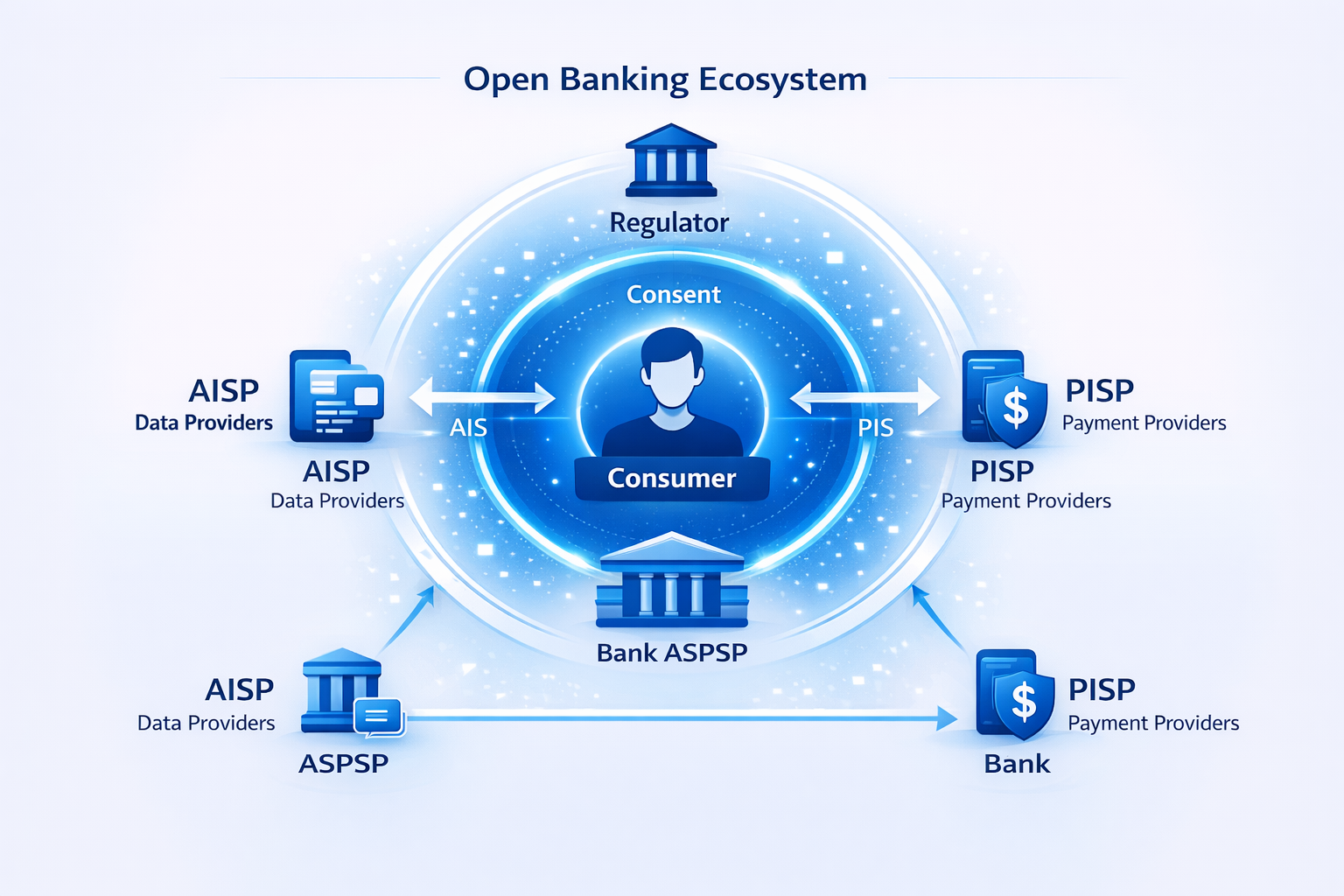

AIS vs PIS: Two Sides of Open Banking

Understanding the distinction between Account Information Services (AIS) and Payment Initiation Services (PIS) is essential:

Key Takeaway

AIS lets apps read your financial data; PIS lets apps move your money. Both require your explicit consent and bank-grade authentication.

Who Are the Key Players in Open Banking Ecosystems?

Open banking involves several types of regulated entities, each playing a specific role:

1. ASPSPs (Account Servicing Payment Service Providers)

These are the banks and financial institutions that hold customer accounts and provide the APIs. They are the data source. Examples include high-street banks, neobanks, and building societies. Under PSD2, ASPSPs are legally required to provide API access to licensed third parties.

2. AISPs (Account Information Service Providers)

AISPs are licensed to access customer account information through open banking APIs. They power applications like budgeting tools, account aggregators, and credit scoring platforms. AISPs can view account data but cannot move money. Examples include personal finance apps that consolidate multiple bank accounts into a single dashboard.

3. PISPs (Payment Initiation Service Providers)

PISPs are licensed to initiate payments on behalf of the customer directly from their bank account. This enables instant bank-to-bank transfers without needing a card. PISPs power use cases like e-commerce checkout, bill splitting, and B2B payments.

Key Takeaway

ASPSPs (banks) provide the data and payment rails. AISPs read data. PISPs initiate payments. All must be licensed by financial regulators like the FCA (UK), BaFin (Germany), or equivalent national authorities.

Open Banking API vs BaaS vs Embedded Finance Which Wins?

These three terms are often confused. Here is how they differ:

Open banking is the foundational layer. BaaS builds on top of it by offering full banking capabilities as a service. Embedded finance takes those capabilities and places them inside non-financial products and customer journeys.

What Real Open Banking API Use Cases Generate Revenue?

In digital finance, friction often appears where platforms depend on outdated or disconnected data. Open banking APIs reduce that friction by enabling real-time access to verified financial information.

Here are five practical use cases showing how:

1. Bank-connected accounting software

Many businesses still rely on outdated methods to keep accounts updated. Exporting transaction statements and uploading them manually remains common across small finance teams. With open banking APIs, platforms connect directly to authorised accounts through a secure integration. Approved data flows automatically, making reconciliations more reliable and far less time-consuming.

2. Faster credit evaluation for lending platforms

Legacy credit checks often exclude applicants who don’t meet traditional scoring models. By integrating open banking, lenders access live account data with user permission. They evaluate spending behaviour, income trends, and balances in real time. It allows better decision-making, especially for borrowers with thin or evolving credit profiles.

3. Simplified mortgage pre-qualification

Mortgage platforms often request lengthy financial documents before processing an application. When connected through open banking, applicants can share verified income and transaction data instantly. It reduces back-and-forth and lowers drop-off from those unable to submit documents on time. It also helps lenders confirm key details faster and more reliably.

4. Live monitoring for fraud detection

Security teams benefit from behavioural signals that reflect current user activity. Open banking APIs support this by enabling real-time checks during high-risk events. Inconsistent patterns, such as unknown devices or abnormal spending, can trigger immediate action. That helps platforms catch fraud before exposure widens or funds are moved.

5. Direct payments without third-party processors

Platforms looking to control payment flow use open banking to initiate bank-to-bank transfers. Once authorised, the transaction executes within the connected system securely and transparently. It reduces reliance on card networks and lowers payment processing costs significantly.

What Benefits Justify Open Banking API Costs?

For Banks

- New revenue streams: Monetise APIs through premium data access, tiered usage plans, and partner integrations.

- Improved customer retention: Banks that enable open banking become a platform, not just a product. Customers stay because the bank is the hub of their financial ecosystem.

- Regulatory compliance: PSD2, CDR, and other mandates require API access. Early compliance turns a regulatory burden into a competitive advantage.

- Operational efficiency: APIs reduce the cost of partner integrations, data sharing, and payment processing compared to legacy methods.

For Fintechs

- Faster product development: Standardised APIs eliminate the need to build bespoke integrations with each bank.

- Reach underserved markets: Access to real banking data enables credit scoring for thin-file customers who lack traditional credit histories.

- Reduced payment costs: PIS-based payments avoid card network interchange fees, reducing costs by 50-80%.

- Data-driven personalisation: Transaction data enables hyper-personalised product recommendations and pricing.

For Consumers

- Greater control over data: Consent-based sharing means users decide exactly who sees what and for how long.

- Better financial products: Competition drives innovation, leading to lower fees, better rates, and more personalised services.

Seamless experiences: One app to view all accounts, one-click payments, instant loan approvals.

Why Can't I Ignore Open Banking APIs in 2026?

For decades, banks treated customer data as something to protect by locking it away. That worked when people did everything through a single institution. But today, users manage money across platforms, apps, and services. Open banking APIs finally give banks a way to meet that reality without compromising trust or control.

Here’s why that shift matters, both for institutions and everyone they serve.

1. Enables faster product development

Without APIs, financial products often take months to build or integrate. Open access to core systems makes development cycles faster, cleaner, and more scalable. Teams don’t have to replicate infrastructure. They can connect to what’s already trusted and tested. That is why fintech startups can move quickly while banks remain competitive.

2. Connects experiences end-to-end

People expect consistency between the tools they use, especially when money is involved. Open banking allows those tools to speak the same language using live financial data. That is how a budgeting app pulls real-time balances or a lender checks income instantly. The more connected the experience, the less users have to think about it.

3. Reaches underserved markets

Not every user fits into traditional banking boxes. Freelancers, microbusinesses, and gig workers often struggle to access useful financial services. Through APIs, banks can work with platforms already tailored to those needs. That expands access without requiring new infrastructure or dedicated product lines.

4. Cut manual overhead

Too much banking still relies on paperwork and internal coordination. APIs automate parts of the process, like verifying identity, pulling account history, or triggering payments. The result is speed, accuracy, and consistency. Staff spend less time fixing errors and more time solving real problems.

5. Opens up revenue models

When APIs are treated as business tools instead of background systems, they generate value. Banks can offer usage-based access to data, payments, or verification layers. This model does not rely on interest or physical expansion. It treats infrastructure as something others can build on for a price.

6. Improves everyday decision making

With APIs, decisions are not based on outdated or incomplete information. Whether it is credit scoring or fraud detection, data flows in real time. That helps institutions respond to what is happening instead of what has already passed. Good data leads to faster action, fewer mistakes, and stronger user confidence.

Curious how open banking is evolving? Dive into our latest insights and predictions in Open Banking in 2025: Key Trends, Use Cases & What’s Next

Core components of the open banking API

Open banking APIs rely on more than just endpoints and developer access. And behind every secure connection is a coordinated system of infrastructure, permissions, and governance. Each part works together to enable safe, efficient, and compliant data exchange across financial institutions and third-party providers.

Here’s a look at the foundational components:

1. API management platform

The API management platform handles how APIs are delivered, secured, and maintained.

- API Gateway: This is the entry point for every API request. It manages traffic flow, validates tokens, and filters requests for security and efficiency.

- Operations Management: Over time, APIs must evolve without disrupting services. Version control, monitoring, and policy enforcement all fall under this operational layer.

- Consumption Management: Third-party developers need clear access to documentation, testing environments, and authentication tools. A consumption layer handles onboarding and ongoing developer support.

- Service Mesh: Within a banking system, multiple services often interact behind the scenes. A service mesh allows APIs to connect internally while maintaining observability and control across services.

2. Consent management platform

Consent isn’t just a feature in Open Banking; it’s the foundation. It ensures customers control when and how their data is shared.

- Consent Collection: The system captures each user’s permission with clarity, like what data is shared, with whom, and for how long. This step ensures transparency before anything leaves the bank’s servers.

- Consent Tracking: It’s not enough to collect consent once. The platform keeps a real-time record, so users can revoke access or adjust preferences at any time.

- Data Processing

Only approved data flows through the system. This layer enforces limits automatically and makes sure no extra or unauthorised data is exposed or used.

3. Security infrastructure

Open banking relies on a stable, secure foundation. Every connection, transaction, and API request must meet the highest level of protection.

- Strong Authentication: Each session begins with secure identity verification. Protocols like OAuth 2.0 and OpenID Connect check both the user and the third-party provider.

- Data Encryption: All data is encrypted while moving and while stored. TLS handles transmission security. AES protects what sits in systems, databases, or cloud storage.

- Rate Limiting: APIs set firm boundaries on traffic volume. Rate limits prevent excessive or suspicious calls from harming system performance or availability.

- API Versioning: Banks need to update APIs without breaking existing tools. Versioning helps preserve functionality across older connections while introducing better security controls.

- Security Audits and Compliance: Testing doesn’t stop after launch. Ongoing audits surface vulnerabilities and help meet standards like PSD2 and GDPR.

Concerned about compliance or data integrity? Explore best practices in our detailed guide on Open Banking Security

4. Developer Portal

A self-service portal where third-party developers can discover APIs, read documentation, test in sandbox environments, and manage their credentials. A great developer experience accelerates partner onboarding and ecosystem growth.

DigitalAPI.ai’s multi-gateway API management platform provides all four components out of the box: centralised API gateway management, built-in consent workflows, enterprise-grade security, and a customisable developer portal. Book a demo to see how it works for your open banking initiative.

Security and Authentication for Open Banking APIs

Security is the backbone of open banking. Every API call involves sensitive financial data or payment instructions, so the security framework must be multi-layered:

1. OAuth 2.0 and OpenID Connect

The standard authorisation framework for open banking. OAuth 2.0 issues access tokens that grant specific, scoped permissions. OpenID Connect adds an identity layer, verifying the user’s identity alongside their permissions. Tokens are short-lived and must be refreshed, limiting the damage if one is compromised.

2. Strong Customer Authentication (SCA)

Required by PSD2, SCA mandates that electronic payments use at least two of three factors: something the customer knows (password/PIN), something they have (phone/hardware token), and something they are (fingerprint/face). SCA applies to every PIS transaction and to AIS onboarding.

3. Mutual TLS (mTLS)

Standard TLS encrypts data in transit, but mTLS goes further: both the client and server present certificates and verify each other’s identity. This prevents man-in-the-middle attacks and ensures that only registered, legitimate TPPs can connect to bank APIs.

4. Dynamic Client Registration

Instead of manually onboarding each TPP, banks can use dynamic client registration (DCR) to allow TPPs to register programmatically. The TPP presents its regulatory credentials (e.g., eIDAS certificate), and the bank’s API platform automatically provisions API access.

5. OWASP API Security Top 10

Best-practice security for APIs includes protection against broken object-level authorisation, injection attacks, excessive data exposure, and rate-limiting abuse. Every open banking API platform should be audited against the OWASP API Security Top 10 checklist.

Key Takeaway

Open banking APIs are secured by multiple overlapping layers: OAuth 2.0 for authorisation, SCA for authentication, mTLS for transport, and consent management for data governance. This makes them significantly more secure than legacy screen scraping.

Global Open Banking API Standards & Frameworks

Open banking regulation varies significantly by region. Here is how the major frameworks compare:

PSD2 Deep Dive

PSD2 is the most influential open banking regulation globally. Key provisions include:

- Mandatory API access: Banks must provide free API access for AIS and PIS to licensed TPPs.

- Strong Customer Authentication: Two-factor authentication for electronic payments and account access.

- Consumer protection: Liability shifts to banks for unauthorised transactions, with refund rights for consumers.

- Passporting: A licence in one EU member state is valid across all EEA countries.

The upcoming PSD3 (expected 2025-2026) will further strengthen the framework by addressing API performance issues, expanding the scope, and improving consumer protection measures.

India’s Account Aggregator Framework

India’s approach is unique. Rather than mandating bank APIs directly, the RBI created the Account Aggregator (AA) framework, which introduces a new type of regulated entity that sits between data providers (FIPs – Financial Information Providers) and data consumers (FIUs – Financial Information Users). AAs handle consent management and data routing but never store data themselves, creating a privacy-preserving architecture.

Open Banking API Architecture

How you architect your open banking APIs has a direct impact on performance, scalability, and compliance. There are two primary models:

1. Centralised Gateway Architecture

All API traffic routes through a single, centralised API gateway. This model provides a unified control point for security policies, rate limiting, analytics, and version management. It is simpler to manage but can become a bottleneck at scale.

- Best for: Banks with a manageable number of API partners and moderate traffic volumes.

- Risk: Single point of failure if not designed for high availability.

2. Distributed / Federated Architecture

API gateways are deployed across multiple regions or business units, each managing its own subset of APIs. A central control plane provides governance and policy consistency across all gateways. This model scales horizontally and reduces latency for geographically distributed consumers.

- Best for: Large banks with multi-region operations, high transaction volumes, or multiple business lines.

- Risk: Greater operational complexity; requires strong governance tooling.

How to choose the right API and integrator

Choosing the right API and integration partner influences product stability, delivery time, and long-term adaptability. It impacts technical teams, compliance workflows, and overall business performance.

Here are the core factors to consider while making that decision:

1. Return on investment

Assess the impact on time-to-market, operational workload, and internal development costs. Strong APIs reduce engineering hours by offering well-documented, ready-to-deploy endpoints. Ask what measurable improvements the provider delivers in speed, efficiency, and delivery cost.

2. Ownership and maintenance costs

Initial pricing tells only part of the story. Review long-term costs tied to maintenance, upgrades, scaling, and developer onboarding. A capable provider should support infrastructure compatibility and minimise toolchain sprawl.

3. Scalability and flexibility

Ensure the solution can handle growth without disruption. Ask how the system performs across geographies, multiple environments, and different volume classes. The right provider should show examples of handling concurrent load without redesigning the system.

4. Operational reliability

Look for clear uptime guarantees, resolution timelines, and support quality. Ask about average response times, escalation protocols, and transparency during incidents. Reliable partners support stability without creating service bottlenecks.

5. Developer enablement

Good documentation reduces internal handoffs and development cycles. Check if their APIs offer consistent patterns, authentication samples, and sandbox availability. A complete onboarding package often signals stronger internal discipline.

6. Security and compliance alignment

Confirm the provider supports regional frameworks like PSD2, CDR, or GDPR. Ask how they handle user revocation, scope limitation, and audit logs. They should offer data governance alignment without manual intervention from your end.

Integrate your APIs for banking effectively with DigitalAPI

APIs shape how banks build, scale, and deliver digital financial services. A well-structured integration allows teams to move faster without compromising performance, compliance, or user experience. That’s where a consistent, governed approach to API delivery becomes a business advantage.

When banking systems grow, integration challenges usually follow. Teams often work across disconnected platforms, manage scattered documentation, or duplicate efforts during onboarding. To solve this, integration must support change while keeping things stable across teams and timelines.

DigitalAPI helps financial institutions simplify and control the full open banking API lifecycle. From developer onboarding to consent tracking, they offer the tools to unify every part of the process.

Ready to Build Your Open Banking API Platform?

DigitalAPI.ai provides a multi-gateway API management platform purpose-built for banking and fintech. Manage, secure, monetise, and scale your open banking APIs from a single control plane.

Book a Demo!

Frequently asked questions

1. What does an Open Banking API mean?

An Open Banking API refers to a secure way for authorised third parties to access customer-approved financial data. It is the process of linking banking systems with everyday digital tools so businesses can automate payments, speed up lending checks, improve fraud detection, and manage accounting in real time. This helps teams work faster with fewer manual steps

2. How are Open Banking APIs regulated globally?

Regions follow different rules: Europe (PSD2), UK (Open Banking UK), Australia (CDR), India (Account Aggregators). Each sets standards for security, consent, and data access.

3. . What is the difference between API Banking and Open Banking?

API Banking refers to banks exposing services to partners through APIs. Open Banking is broader: it mandates banks to share customer data (with consent) to third parties, enabling more innovation.

4. What challenges exist in implementing Open Banking APIs?

Banks face technical integration issues, regulatory compliance costs, inconsistent standards across regions, and the need to build trust with consumers.

5. Are Open Banking APIs safe to use?

Yes, security is built into the framework. APIs rely on encryption, tokenisation, and strict regulations like PSD2 in Europe or RBI’s Account Aggregator model in India to ensure safe data sharing.

Dhayalan Subramanian is Associate Director, Product Growth at DigitalAPI, where he leads go-to-market and product growth for the company’s multi-gateway API management platform. His work focuses on helping large enterprises and mid-market cloud companies consolidate APIs across AWS, Azure, Apigee, Kong, MuleSoft, and other gateways into a single control plane for governance, discovery, monetization, and agent consumption.

Dhayalan brings 14+ years of experience across product strategy, enterprise architecture, and engineering leadership. Earlier in his career, he held senior roles at Encora (as Associate Architect and Technical Manager), Mindtree (Technology Lead), Tech Mahindra (Technical Lead), and Primus Analytics, where he designed integration frameworks and delivered enterprise-grade digital platforms for global customers.

At DigitalAPI, he works directly with platform, integration, and developer experience leaders at Fortune 500 organizations to operationalize unified API catalogs, developer portals, and MCP-ready APIs. He writes regularly on API developer experience, API governance, and AI agent architectures.

One email a fortnight. Worth opening.

A short digest of what we're writing, what we're learning from customers, and the handful of links you'd actually want from us. No tracking pixels.

.avif)