Webinars

Featured Blog

J.P. Morgan just flipped the switch on API economy: Are your APIs ready?

J.P. Morgan Chase, the largest U.S. bank by assets, shocked the fintech world by announcing it would begin charging third-party platforms and data aggregators for access to its customers’ bank account information.

J.P. Morgan’s decision to charge for API access marks a turning point, APIs are no longer free infrastructure but strategic, monetizable products. This shift will push every bank and enterprise to adopt commerce-grade SLAs, centralised catalogues, and compliance-first workflows, redefining APIs as direct revenue drivers rather than technical utilities.

DigitalAPI helps organisations prepare for this new era by giving them full visibility into their API estate, enforcing governance, and enabling external monetisation. With automated discovery, secure marketplaces, self-serve sandboxes, and analytics, DigitalAPI transforms APIs into revenue-ready products, helping enterprises turn data access into their next competitive advantage.

Streamline your API Monetization journey with DigitalAPI—Book a Demo!

On July 11, 2025, J.P. Morgan Chase, the largest U.S. bank by assets, shocked the fintech world by announcing it would begin charging third-party platforms and data aggregators for access to its customers’ bank account information.

Until now, the free (or nominal-fee) flow of transaction data through intermediaries like Plaid and MX has underpinned the rapid rise of budgeting apps, lending platforms, and payment services.

By distributing formal pricing sheets to aggregators and signalling higher fees for payment-focused use cases, JPMorgan has effectively “flipped the switch” on what had been an implicit, infrastructure-subsidy model.

What does this mean for APIs, and why does it change everything?

From here on out, APIs won’t just be a technical convenience; they’ll be direct profit centres, complete with SLAs, tiered pricing and usage monitoring. Fintechs that built their business models on “free” data will face sudden cost pressure, and banks that haven’t yet thought of their APIs as products will scramble to catch up. You can expect three seismic shifts:

- Commerce-grade SLAs & billing: Every endpoint will need clear uptime guarantees and metered billing.

- Centralised API catalogues: Organisations must know exactly which APIs they own, who’s using them, and how profitable each is.

- Compliance-first workflows: KYC, legal approvals and sandbox-to-production gates will become table stakes in any API marketplace

Why API monetisation is the next competitive battleground

APIs have evolved far beyond their original role as “plumbing” for internal systems. Today, they’re strategic products that can drive new revenue streams, foster ecosystem growth, and create lasting differentiation. Here’s why the race to monetise APIs will define winners and losers in every industry:

1. APIs as product lines

Just like traditional products, APIs can be versioned, tiered, and marketed to different customer segments. Charging for access forces organisations to think about design, packaging, and user experience, transforming APIs from technical artefacts into profitable offerings.

2. New revenue streams & recurring income

Usage-based or subscription pricing on high-value data and services (e.g., account information, payment initiation, risk scoring) unlocks ongoing revenues. Firms that crack the right pricing model can build predictable, recurring income rather than one-off projects.

3. Ecosystem stickiness & network effects

When partners integrate deeply with your paid APIs, they become “locked in” to your ecosystem. Over time, this drives cumulative network effects: more partners attract more customers, which in turn invites more partners, and it all hinges on a well-managed, monetised API marketplace.

4. Differentiation through developer experience

In a world where multiple providers may offer similar data or services, developer experience becomes a key competitive lever. Clear documentation, self-service sandboxes, robust SLAs and transparent billing give one API provider a decisive edge over another.

5. Data as a strategic asset

Charging for API access signals that your organisation views its data not merely as a by-product but as a core asset. This mindset shift encourages better governance, quality controls, and compliance workflows, all of which strengthen trust and long-term partner relationships.

6. Pressure on lagging firms

As leading institutions (like JPMorgan) put formal price tags on APIs, rivals that still treat APIs as “free” or secondary will lose out. They’ll attract fewer integration partners, struggle to recoup infrastructure costs, and ultimately forfeit market share to more forward-thinking competitors.

Six Signals that your API portfolio is not ready for monetisation

To turn your APIs into profitable products, you need clear indicators that your portfolio is primed for external consumption, billing and scale. Here are the six key signals to look for:

1. Discovery & cataloguing

Signal: You do not have any internal centralised registry that lists every API, its business domain, maturity level and target audience.

Why it matters: You can only monetise what you know exists. A comprehensive API catalogue lets you identify high-value endpoints, eliminate API sprawl, and earmark them for external access.

2. Inconsistent documentation

Signal: Your APIs are not up-to-date, auto-generated specs and interactive “try-it-now” docs.

Why it matters: Developers evaluating a paid API need to onboard in minutes, not days. High-quality docs reduce friction, lower support costs, and accelerate partner launches.

3. Governance & monitoring

Signal: You don’t have enforced SLAs, quota limits, security policies and compliance checks across all APIs.

Why it matters: Monetisation demands accountability as partners expect guaranteed uptime, predictable performance and strict data-privacy controls, especially in finance, healthcare or telecom.

4. External marketplace

Signal: You don’t have a unified, branded storefront where third parties can discover, subscribe to, and pay for your APIs.

Why it matters: An external-facing marketplace signals maturity to partners, simplifies discovery, streamlines onboarding, and enables pricing experimentation, usage-based billing, and revenue tracking.

5. Self-service sandboxes & test environments

Signal: Lack of realistic test environments that support open banking and other compliances, where partners can prototype against transactional data without risk, can lead to a poor developer experience.

Why it matters: A frictionless sandbox is the gateway to paid adoption. It lets partners validate integrations, build demos and prove business value before committing dollars.

6. Pricing strategy & tiering

Signal: Unclear pricing models without any tiers (usage-based, subscription and freemium tiers) that align value with cost.

Why it matters: The right pricing unlocks revenue without scaring off early adopters. Tiered plans let you cater to both startups seeking trial access and enterprises needing high-volume SLAs.

How does Digital API help you monetise your APIs?

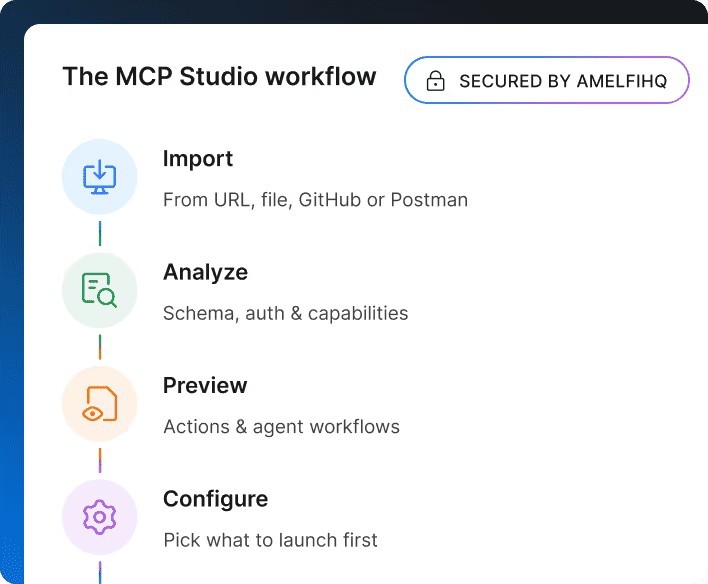

Digital API helps you lay the groundwork needed before monetisation can even begin, starting with API visibility and control. It automatically discovers and catalogues all your APIs across gateways and business units, reducing duplication and surfacing high-value assets. With this foundation, it becomes easier to enforce governance, implement security policies, and identify which APIs are ready for external consumption.

Once your internal API portfolio is structured and governed, Digital API lets you launch an external marketplace built as per your needs, where partners can discover, subscribe to, and test your APIs through a seamless self-serve experience. This includes sandbox environments, open banking-compliant workflows, and analytics to track adoption and usage.

Bharath Kumar is the Founder and CEO of DigitalAPI, the multi-gateway API management platform helping organizations unify API discovery, governance, monetization, and AI agent enablement across Apigee, AWS, Azure, Kong, and MuleSoft.

Bharath founded DigitalAPI in 2015 after several years as a Solutions Architect at Apigee, the platform now part of Google Cloud and widely regarded as the foundational product of the modern API management category. At Apigee, he worked across pre-sales, product evangelism, and customer architecture, designing API programs for Fortune 100 customers. Earlier in his career, he held engineering roles at IBM, GalaxE Solutions, and Infinite Computer Solutions.

Under his leadership, DigitalAPI has grown into a globally recognized API management platform and caters to multiple Fortune 500 customers. His perspective on APIs, AI, and developer experience has been featured in Forbes, and he is a recurring speaker at Apidays and other API industry events.

One email a fortnight. Worth opening.

A short digest of what we're writing, what we're learning from customers, and the handful of links you'd actually want from us. No tracking pixels.

.avif)